- Fabrick, through its subsidiary Axerve, which specialises in providing accessible and frictionless payment solutions for Ecommerce and physical sales, released a new whitepaper today that explores the market penetration of alternative payment methods across a variety of geographies and industries.

- In exclusive company data, Axerve found that PayPal is the method with the largest volumes, reaching 59% of the overall alternative payments. This is followed by MyBank, with 25%, and Sofort by Klarna, which accounts for 3% of the total collections with methods other than credit cards.

- In the UK digital payments sector the total transaction value is forecast to reach almost $440 billion in 2023.

Milan, April 20, 2023 – Fabrick, a European leader in open finance, and its subsidiary Axerve, Payment Partner to Grow, a provider of accessible and frictionless payment solutions for ecommerce and physical sales, announce today the release of a new whitepaper, “Alternative payment solutions: how they are changing the payment scene.” This whitepaper explores the ways in which alternative payments are revolutionising traditional banking.

In many cases, alternative payments provide an easier and more efficient way to make payments.

Alternative payment solutions respond to the specific needs of today’s market, both in terms of user experience and the checkout process. By providing local demographics with the opportunity to pay with their preferred and most commonly used methods of payment, merchants can take advantage of transparent fee conditions, often without hidden costs, as is the case with digital wallets. Moreover, alternative payments offer many benefits for consumers, such as convenience, ease of use, and better accessibility compared to traditional methods.

The world of alternative payments refers to everything that falls outside of the traditional payment methods that have been used both for online and in-store purchases, specifically all the payment solutions alternative to the main credit/debit card networks, cash, and checks. Alternative payments are on the rise both in the Ecommerce and physical stores landscape and projected to reach more than $15.000 billion by 2027, with a CAGR of 16.3% over the period 2017- 2027[1]. This growth has been triggered by the increasing needs of merchants to follow the expansion of Ecommerce across the world, the inability of traditional payments to meet the buyer’s needs, and the complexity around the checkout process vis-à-vis the fast and frictionless types of technological experience that were arising in the digital payments’ world.

The new whitepaper from Axerve dives into the evolution of alternative payment methods and analyses the market penetration of different types of methods, such as digital wallets, account-to-account transfers, Buy Now Pay Later options, and cryptocurrencies. According to Axerve’s customer analysis, that was performed in 2023, digital wallets remain the most widely used payment methods across the world, however, Buy Now Pay Later platforms and A2A (Account-to-Account) tools, such as iDEAL and MyBank, are gaining traction. PayPal still holds the highest market share, accounting for 59% of the overall alternative payments. MyBank follows with 25%, and Sofort by Klarna accounts for 3% of the total collections with methods other than credit cards.

Axerve’s pool of clients demonstrates that the adoption of alternative payments is widespread across all market sectors, from Fashion to Food & Beverage. In particular, the Fashion sector has seen the most integrations of alternative payment methods, with Klarna achieving transaction volumes of over 54%.

Despite the fact that two-thirds of the UK population believe cashless methods are riskier and more prone to fraud than cash, the current statistics and tendencies suggest otherwise. In 2021, one third of the population barely used cash, and total transaction value in the UK digital payments sector is forecast to reach almost $440 billion in 2023. Furthermore, the UK is one of the most cashless countries in the world, with 95% of people having internet access, 97% having a bank account, and 65% being credit card owners.

Moreover, card payments make up more than half of all payments (51%) and alternative payment methods make up 41%. Bank transfers make up 7%, while cash is only responsible for 1%. These figures make it clear that the UK is swiftly progressing towards a cashless economy.

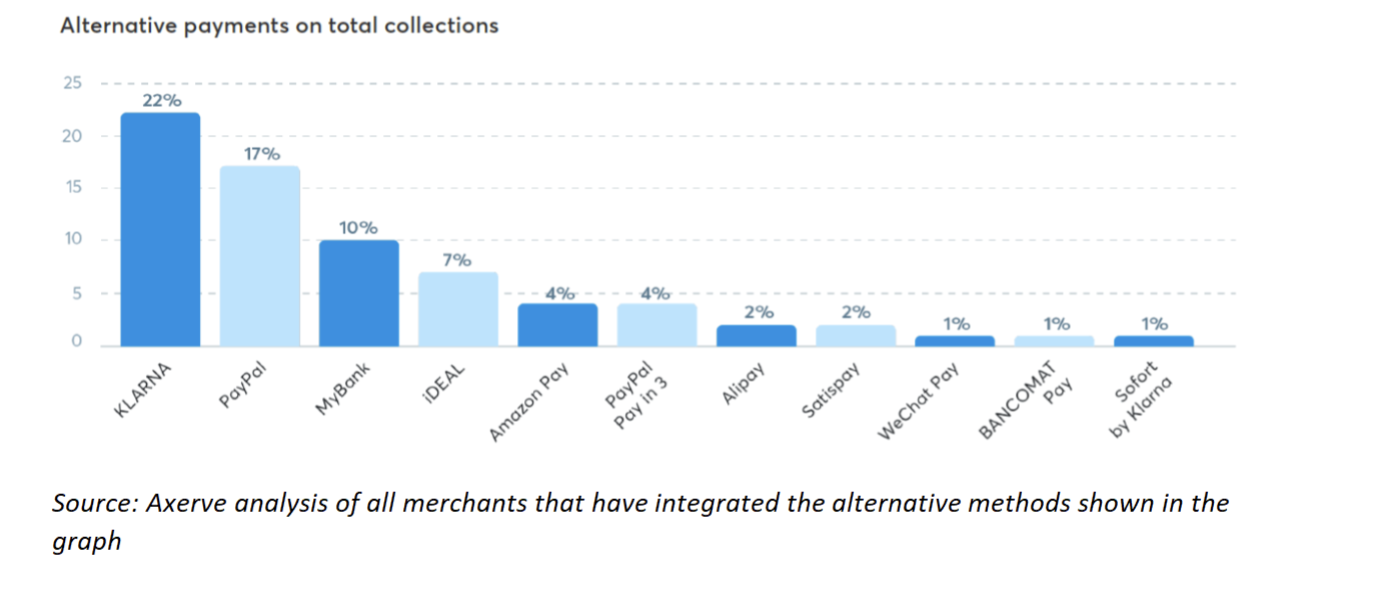

By comparing the transaction value of the individual methods to the total amount collected by ecommerce merchants that have integrated those specific alternatives (it must be considered that merchants may have implemented one or more alternative payments with a direct integration, i.e. without going through the Axerve-managed flows), it is Klarna, in its instalment payment formula, that registers the highest penetration in comparison to total collections (22%), followed by PayPal, which is confirmed as the most widely used digital wallet across all sectors. Among the A2A forms of payment, it is MyBank and iDEAL that account for the most, 10% and 7% respectively, while Satispay and Sofort by Klarna record only 2% and 1% of the total volumes collected by the Ecommerce shops that have integrated them.

The Axerve whitepaper on all the different types of alternative payments, with specific insights on global and local penetration is available at the link.

“The market penetration of alternative payments continues to grow steadily in various geographies and across several product sectors around the world, displacing traditional payment methods,” said Alessandro Bocca, CEO at Axerve. “Going forward, we anticipate a further development of alternative payment solutions, which will require merchants to adopt collection platforms capable of managing the wide array of solutions available. This includes not only the payment solutions themselves but also their underlying supply chain of services, such as acquirers, fraud prevention and integrated alternative payments. To succeed in this environment, merchants must be ready to act quickly and optimise their sales and minimise costs.”

“Consumer demand for alternative payment solutions shows a continued appetite for more innovative, digital payment solutions,” said Paolo Zaccardi, Co-Founder and CEO of Fabrick. “Digital payments continue to grow in popularity and the sheer variety of payments options out there means that easy payment integrations have become extremely important for business.

“At Fabrick, via the subsidiary, Axerve, we are committed to providing our customers with the most innovative and secure alternative payment solutions in an ever-evolving digital world. We are proud to be at the forefront of the Open Finance revolution and to be able to offer merchants the most efficient and secure payment solutions available. Our whitepaper, “Alternative payment solutions: how they are changing the payment scene”, highlights the various ways in which alternative payments are revolutionising the customer journey.”

Axerve plays a pivotal role in the alternative payments solutions industry, covering the entire payment service value chain from technological platforms to financial services and merchant relationship management. Its proprietary Payment Orchestra™ simplifies payment acceptance to reduce shopping cart abandonment rates and increase sales opportunities. Additionally, Axerve develops omnichannel cross-selling dynamics to create an individualised and satisfying shopping experience. Customers can accept any type of payment in a secure, clear, and simple way through physical and digital gateways such as POS, ecommerce solutions and cashin machines. In September 2022, Axerve published a whitepaper on payment orchestration which assessed the positive impact that it is having on merchants through higher payment authorisation and cost-effective, streamlined checkout mechanisms.

***

Fabrick

Fabrick is a European pioneer in Open Finance. Headquartered in Milan and with offices in London, Madrid and Zurich, it operates internationally to enable innovative services in Open Finance by supporting the collaboration of fintechs, businesses and financial institutions.

Fabrick’s technological platform and ecosystem of relationships enables the development of new business models in finance, fostering growth and opportunities for all participants and delivering the concrete advantages of innovation to the end customer, either consumer or business.

Fabrick has embedded platform services into many solutions to address different use cases, from open banking to open payments and beyond. Fabrick, together with its subsidiary Axerve, provides payment orchestration services, as a payment facilitator and global payment gateway aggregator, and Open Banking services through its license as Account Information Service Provider (AISP) and Payment Information Service Provider (PISP) passported to 11 countries in Europe.

Fabrick presents the new way of doing finance: open, modular, and data-driven and takes this approach to all aspects of the financial ecosystem. For financial institutions, Fabrick represents an ecosystem of innovative services. For fintechs, the network effect created by Fabrick is the opportunity to leverage an open platform infrastructure of partners and services. For corporates, Fabrick is where to find tailor-made solutions to innovate customer journeys.

Press contact

Tancredi Intelligent Communication:

Helen Humphrey – M +44 7449 226720, [email protected]

Benedetta Barelli – [email protected]

Dasha Korznikova – [email protected]

Fabrick:

[1] FinTech- In-depth Market Insights & Data Analysis / Statista 2022