Customer disputes are a huge pain point, but types of fraud that can be at the root of them are not widely understood. Most of us are familiar with true fraud (also called identity theft) and we’ve used front-end fraud protection to safeguard against it.

Chargeback fraud and friendly fraud, however, are very different from true fraud and even one another. Understanding the types of fraud and their clear differences gives you the opportunity to protect your business and customer relationships.

Cementing Fraud’s 3 Definitions

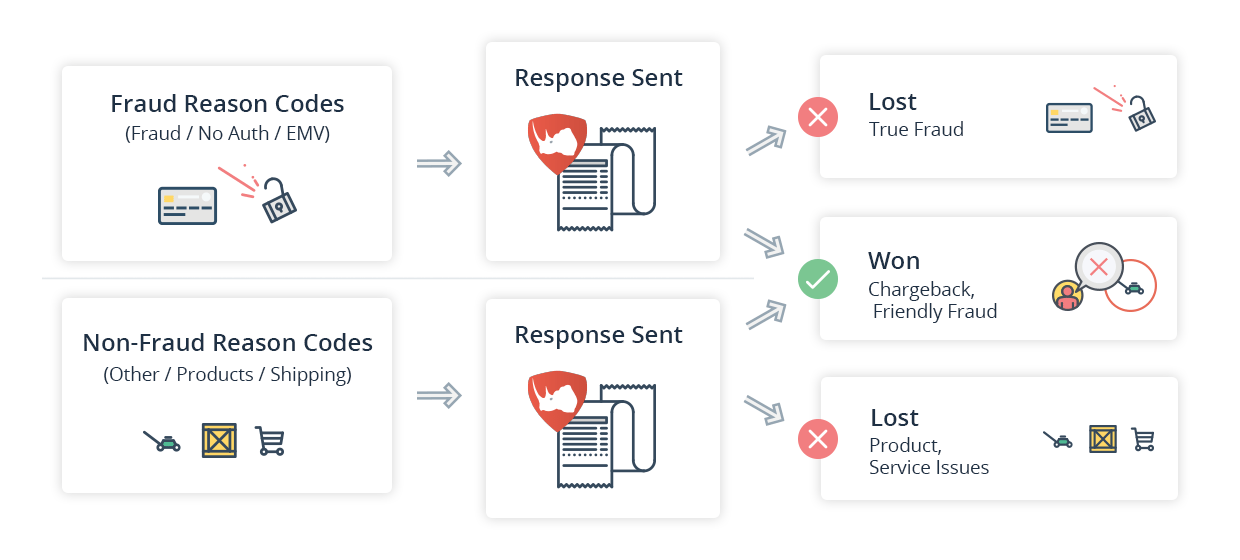

Fraud experienced by your business comes in three forms: true fraud, chargeback fraud, and friendly fraud. All of which appear to businesses as customer disputes, or chargebacks.

When you receive a chargeback, it’s categorized under either fraud reason codes or non-fraud chargeback reason codes. But the only way to actually reveal the chargeback’s cause (and what type of fraud your business is experiencing) is through submitting a chargeback response with the right compelling evidence.

After you submit a response, the issuing bank decides whether or not the chargeback is valid. Valid chargebacks are the result of true fraud and product or service issues. Invalid chargebacks, or chargebacks you ‘win’, represent cases of chargeback fraud or friendly fraud.

True Fraud

True fraud, also called identity theft, occurs when your business accepted payment from a stolen card. The customer disputes the purchase, which results in his or her bank closing the account and issuing a new account number and card to the customer.

Chargeback Fraud

Both chargeback fraud and friendly fraud involve an invalid use of chargeback rights by a cardholder. But chargeback fraud is a purposeful misapplication of these rights in effort for a customer to ‘have their cake and eat it, too’. The goal of the dispute is to keep the product or service acquired while enjoying a refund of the transaction amount.

Friendly Fraud

A misapplication of chargeback rights isn’t always intentional and malicious. Friendly fraud occurs when a cardholder disputes a purchase because they forgot they made the purchase, another family member authorized the purchase, or even misunderstood the return policy. These customers aren’t trying to be deceitful, and that differentiation is key.

Delineation Between Fraud Types is Critical

Efficient management of the dispute resolution process allows you to see what types of fraud your business experiences. With that information, you’re given the opportunity to improve and optimize existing processes and solutions—providing a measurable impact on your bottom line.

Protecting Your Business

If your business is experiencing high rates of true fraud chargebacks, addressing your front-end fraud solutions is a must. At the very least, you should be using fraud prevention tools like AVS, CVV, and geolocation. If basic tools are deployed and rates of true fraud are still high, consider more advanced preventative measures like biometrics, email verification, or social media validation.

Blacklisting Appropriately

It is not unreasonable to blacklist a customer that has tried to commit chargeback fraud against your business. Especially if the customer has issued chargebacks in the past, even if they were ruled to be true fraud. Engaging in communication with these individuals is important. But if that proves unsuccessful, you should block the ‘problem’ customer from making any further purchases (and causing further losses).

Preserving Customer Relationships

This is where the differentiation between chargeback fraud and friendly fraud carries the most weight. A customer who initiated a dispute on the grounds of friendly fraud should not be blacklisted like chargeback fraud customers. When you win a chargeback, reach out to the customer and discuss the outcome with them. Was the merchant descriptor confusing? Were your terms and conditions displayed clearly? Asking these questions and others will provide you with actionable insights on how you can improve operations moving forward.

As long as you accept payments, you’ll receive chargebacks. An understanding of your business’ chargeback ecosystem will allow you to make insightful operational decisions. An optimized chargeback response process ensures you’re recovering revenue that rightfully belongs to your business.

Scott Stone is CMO at Chargeback