In the fast-moving, unforgiving world of payments, it’s not enough anymore to have a peripheral understanding of the hot topics of the day. An ancient industry that in its infancy could be as simple as “making change” now rewards only those merchants who can accurately predict change – and react faster, smarter and better than the competition.

To make that possible, we have identified five trends you need to understand in the near future in order to succeed.

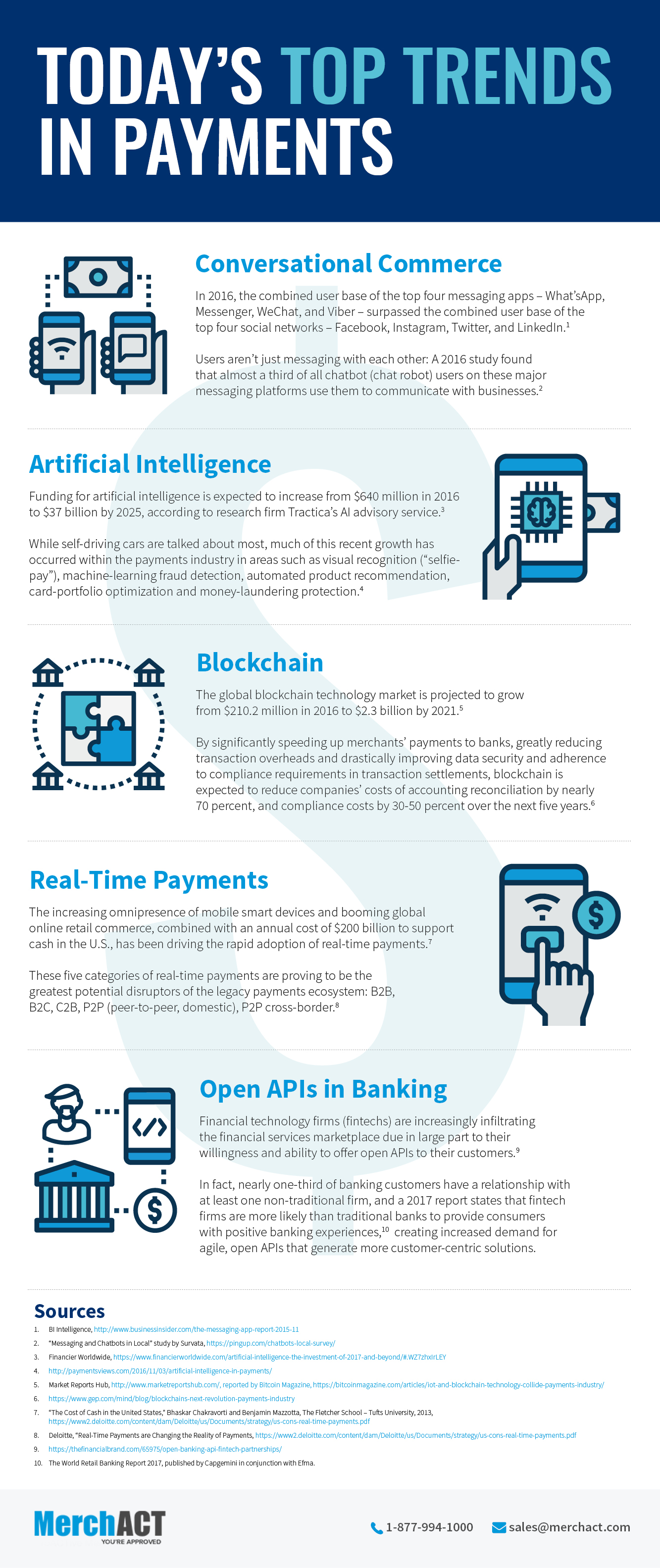

Conversational Commerce

Messaging applications such as WeChat and What’sApp are on the precipice of overtaking social networks including Facebook and Twitter as a means of communication between consumers (see infographic). More importantly for merchants, these apps possess enormous potential as a lucrative, favorite channel for B2C and B2B interactions – including transactions – going forward.

{kind=link}

This trend is already gathering momentum, according to a 2016 survey by Silicon Valley-based brand intelligence research firm Survata. The study revealed that nearly 30% of users of messaging apps powered by chatbot technology are indeed communicating with businesses and not just sharing photos and videos among friends. Nearly 50% of users (55% of millennials) also said using a chatbot to communicate with a business positively influenced their opinion of that business. Finally, 35% of users (52% of millennials) said they would make a business transaction through a chatbot if given the opportunity.

Artificial Intelligence

Artificial Intelligence (AI) is responsible for a number of rapidly developing payments trends to which merchants should be paying close attention. Machine learning (ML) technology that automatically detects payment card fraud is probably the use case with which today’s online business owners are most familiar, as global card fraud reached nearly $22 billion in 2015, according to The Nilson Report. Vendors are increasingly adding ML capabilities to their suites of solutions and it is critical for merchants to be aware of the latest technologies available in their fight against fraud.

Some of the more nascent AI developments in the payments space include facial recognition (“selfie pay”), object recognition (finger and palm prints), motion tracking and voice and event detection, all being explored as payment-authentication tools. Additional developments to watch include automated product recommendations, offer personalization and scheduling optimization.

Blockchain

Another important payments trend is blockchain technology, which was originally developed as a means of more securely trading digital currencies such as Bitcoin. While legacy payments systems are costly and otherwise impeded by centralized money supplies, cumbersome paper transactions, multiple layers of authentication procedures and third-party processors, an open, decentralized blockchain network of transactions can bypass these hurdles while adding another level of security and defraying much of the costs.

Payments are made and received instantaneously on a secure blockchain platform through a globally accessed public ledger, with each transaction becoming a block in the chain that remains permanently visible throughout the network. The lower cost, higher security and seamless compliance process make blockchain an attractive option for alternative payments platforms such as mobile POS systems.

Real-Time Payments

While certainly convenient for consumers, the ability to instantly process card payments greatly benefits merchants in the form of improved transparency, liquidity and overall fund management. What a business lacking in this area may suffer in terms of public perception will inevitably pale in comparison to its actual financial losses from high transaction fees, compromised security systems and limited cash flow.

The U.S. Federal Reserve launched a systematic undertaking in 2015 aimed at improving the global capabilities for real-time payments that will make all domestic and global transactions faster, more secure and more efficient. Any businesses unable to support such an infrastructure will undoubtedly be left behind.

Open APIs

Traditional banking institutions are expending a lot of time and thought into what was virtually unthinkable a decade ago: Opening access to their proprietary financial application programming interfaces (APIs) to outside software developers. The impact on those in the payments industry will be profound in terms of the opportunities presented to the quickest and nimblest of merchants, countered by the limitations experienced by those less able to adopt new technologies.

The open banking trend currently involves different models such as app stores and “sandboxes,” i.e. testing grounds for software code sourced from third parties. This unprecedented access allows outside financial technology firms, many of them startups, to customize their solutions and offer an array of highly personalized products and services – many of which will start emerging in the payments industry.

Jared Ronski is co-founder of MerchACT